Portugal NHR Tax Regime for Digital Nomads (2026 Guide)

Portugal’s Non-Habitual Resident (NHR) tax regime has long been one of Europe’s most attractive fiscal incentives for digital nomads, remote workers, and international professionals. With a 20% flat tax rate on qualifying income and potential exemptions on foreign-sourced earnings, the NHR program offers significant savings compared to Portugal’s standard progressive rates that climb as high as 48%.

TL;DR: Portugal’s NHR regime offers a 20% flat tax rate on qualifying employment and self-employment income for 10 years, with potential exemptions on foreign-sourced dividends, interest, and capital gains. The original NHR closed to new applicants in 2023, but its successor — NHR 2.0 (IFICI) — is available from 2024 onward for professionals in scientific research, innovation, and qualified roles.

In this comprehensive 2026 guide, we break down everything you need to know about the NHR regime — from eligibility requirements and the application process to real-world income examples and a detailed comparison with standard Portuguese taxation. Whether you’re a freelance developer, a remote consultant, or an entrepreneur exploring Portugal as your next base, this guide will help you make an informed decision.

What Is the NHR (Non-Habitual Resident) Regime?

The Non-Habitual Resident regime was originally established under Portuguese Decree-Law 249/2009 to attract skilled professionals, high-net-worth individuals, and retirees to the country. It provides a preferential tax framework for 10 consecutive years from the date of registration.

The NHR regime underwent significant reform in late 2023 and 2024, with the original program being replaced by a revised incentive framework sometimes referred to as NHR 2.0 or the Tax Incentive for Scientific Research and Innovation (IFICI). For 2026, the updated rules apply to new applicants, while existing NHR holders continue under their original terms.

Key Benefits at a Glance

- 20% flat tax rate on Portuguese-sourced employment and self-employment income from eligible “high-value” activities

- Potential exemption on certain categories of foreign-sourced income (dividends, interest, royalties, capital gains, rental income)

- 10-year duration — once granted, the regime applies for a full decade

- No minimum investment required (unlike golden visa programs)

NHR 2.0: What Changed for 2025–2026?

Per the Portuguese Tax Authority (Autoridade Tributária), the Portuguese government replaced the original NHR with the IFICI program (Tax Incentive for Scientific Research and Innovation) effective January 1, 2024 for new applicants. Here is what changed:

- Eligibility narrowed: The new regime focuses on professionals in scientific research, innovation, and qualified positions within certified entities

- Flat rate maintained at 20%: For qualifying employment and self-employment income

- Foreign income treatment: Exemptions remain for income sourced from countries with a Double Taxation Agreement (DTA) or Tax Information Exchange Agreement (TIEA) with Portugal

- Grandfathering: Anyone who obtained NHR status before 2024 retains the original conditions for the remainder of their 10-year period

[!IMPORTANT] If you registered as NHR before January 1, 2024, your existing benefits remain unchanged for the full 10-year period. The new rules only apply to first-time applicants from 2024 onward.

Who Is Eligible for the NHR Regime?

To qualify for the NHR regime (under the 2025–2026 framework), you must meet the following criteria:

- Become a Portuguese tax resident — This typically means spending 183 days or more per year in Portugal, or having a habitual residence in the country as of December 31

- Not have been a Portuguese tax resident in any of the five years preceding your application

- Engage in a qualifying activity — Under NHR 2.0, this includes roles in scientific research, innovation, or positions within entities certified by AICEP (the Portuguese investment agency) or similar bodies

- Register with the Portuguese Tax Authority (Autoridade Tributária e Aduaneira) within the required deadlines

Qualifying “High-Value” Activities

Under the original NHR, a broad list of high-value activities qualified for the 20% flat rate. The updated regime is more restrictive but still covers many roles relevant to digital nomads:

- Software engineers and IT architects

- Data scientists and AI researchers

- University professors and scientific researchers

- Doctors, dentists, and other medical professionals

- Auditors and tax consultants

- Professionals employed by AICEP-certified startups and tech companies

- Roles within industrial and technological free zones

[!TIP] Even if your specific role isn’t on the qualifying list, working for a certified entity (such as a Portuguese tech startup with AICEP certification) can still qualify you for the 20% flat rate.

NHR Tax Rates vs. Standard Portuguese Tax Rates

Understanding the difference between NHR taxation and Portugal’s standard progressive system is crucial. Here’s a side-by-side comparison for 2026:

Standard Progressive Rates (IRS)

| Taxable Income (€) | Marginal Rate |

|---|---|

| Up to €7,703 | 14.5% |

| €7,703 – €11,623 | 21% |

| €11,623 – €16,472 | 26.5% |

| €16,472 – €21,321 | 28.5% |

| €21,321 – €27,146 | 35% |

| €27,146 – €39,791 | 37% |

| €39,791 – €51,997 | 43.5% |

| €51,997 – €81,199 | 45% |

| Over €81,199 | 48% |

NHR Flat Rate

| Income Type | NHR Rate | Standard Rate (Effective) |

|---|---|---|

| Qualifying employment income | 20% | 14.5% – 48% progressive |

| Qualifying self-employment income | 20% | 14.5% – 48% progressive |

| Foreign dividends (from DTA country) | 0% (exempt) | 28% withholding |

| Foreign interest (from DTA country) | 0% (exempt) | 28% withholding |

| Foreign rental income (from DTA country) | 0% (exempt) | 14.5% – 48% progressive |

| Foreign capital gains (from DTA country) | 0% (exempt) | 28% flat |

| Pensions (foreign-sourced) | 10% | 14.5% – 48% progressive |

[!WARNING] Social security contributions are not covered by the NHR regime. Self-employed NHR holders must still pay social security at approximately 21.4% on 70% of their gross income (effective rate of about 14.98% on total income). This is a significant additional cost to factor into your planning.

Real-World Income Examples

Let’s look at how the NHR regime impacts your actual tax bill with concrete income scenarios.

Example 1: Software Developer Earning €60,000/Year

| Scenario | Tax Calculation | Total Tax | Effective Rate |

|---|---|---|---|

| NHR (20% flat) | €60,000 × 20% | €12,000 | 20% |

| Standard rates | Progressive brackets up to 43.5% | ~€16,830 | ~28.1% |

| Annual savings with NHR | €4,830 |

Example 2: Freelance Consultant Earning €100,000/Year

| Scenario | Tax Calculation | Total Tax | Effective Rate |

|---|---|---|---|

| NHR (20% flat) | €100,000 × 20% | €20,000 | 20% |

| Standard rates | Progressive brackets up to 45% | ~€35,490 | ~35.5% |

| Annual savings with NHR | €15,490 |

Example 3: Remote Worker Earning €40,000/Year

| Scenario | Tax Calculation | Total Tax | Effective Rate |

|---|---|---|---|

| NHR (20% flat) | €40,000 × 20% | €8,000 | 20% |

| Standard rates | Progressive brackets up to 37% | ~€9,720 | ~24.3% |

| Annual savings with NHR | €1,720 |

[!TIP] At lower incomes (below ~€30,000), the standard progressive rates may actually result in a lower effective tax rate than the NHR flat 20%. Use our Tax Calculator to model your specific situation before applying.

Step-by-Step Guide: How to Apply for NHR Status

Follow these steps to register as a Non-Habitual Resident in Portugal:

-

Obtain a Portuguese NIF (Tax Identification Number) — You can apply at any local Finanças office or through a fiscal representative if you’re still abroad. This is your essential tax ID for all interactions with Portuguese authorities.

-

Establish tax residency in Portugal — Move to Portugal and ensure you meet the 183-day rule or establish a habitual residence. Sign a rental contract or purchase property to document your address.

-

Register as a tax resident — Update your address with the Finanças office and register as a resident taxpayer. This formally establishes your Portuguese tax residency.

-

Submit the NHR application online — According to the Portuguese Tax Authority’s Portal das Finanças, log into the online platform and navigate to the NHR/IFICI registration section. You must apply by March 31 of the year following the year you became a tax resident.

-

Provide supporting documentation — Upload proof of non-residency in Portugal for the previous five years. This may include tax residency certificates from your former country, rental agreements, or utility bills.

-

Demonstrate qualifying activity — Under NHR 2.0, provide evidence of employment or self-employment in a qualifying high-value activity, or certification from your employer/entity.

-

Await approval — The tax authority will review your application and typically responds within 2–4 weeks. Once approved, the NHR status is applied retroactively to the beginning of your residency year.

-

File your annual tax return — Each year, file your IRS (income tax return) by June 30, declaring your worldwide income and applying the NHR rates to qualifying categories.

[!TIP] Consider hiring a Portuguese tax advisor or contabilista (certified accountant) for the application process. The cost typically ranges from €500 to €1,500 for the full NHR registration, and they can ensure you maximize your exemptions.

Important Deadlines and Costs

| Item | Detail |

|---|---|

| Application deadline | By March 31 of the year after becoming tax resident |

| NIF registration | Free (in person) or €100–€200 (via fiscal representative) |

| NHR application fee | Free (no government fee) |

| Annual tax return deadline | June 30 each year |

| Duration of NHR benefits | 10 consecutive years |

| Social security (self-employed) | ~21.4% on 70% of gross income |

| Social security (employed) | 11% employee contribution |

NHR for Different Types of Digital Nomads

Freelancers and Independent Contractors

As a freelancer under NHR, your Portuguese-sourced self-employment income from qualifying activities is taxed at 20% flat. If you also earn income from foreign clients in countries with DTAs, that income may be fully exempt from Portuguese taxation.

However, you must register as a trabalhador independente (independent worker) and will be subject to social security contributions after your first 12 months.

Remote Employees

If you work remotely for a foreign employer while living in Portugal, your income is generally considered Portuguese-sourced (since you perform the work in Portugal). Under NHR, this employment income can qualify for the 20% flat rate if your role falls within the high-value activities list.

Entrepreneurs and Company Owners

If you operate a foreign company and receive dividends, these may be exempt from Portuguese tax under the NHR regime, provided the income is sourced from a country with a DTA with Portugal and could be taxed in that country under the treaty’s rules.

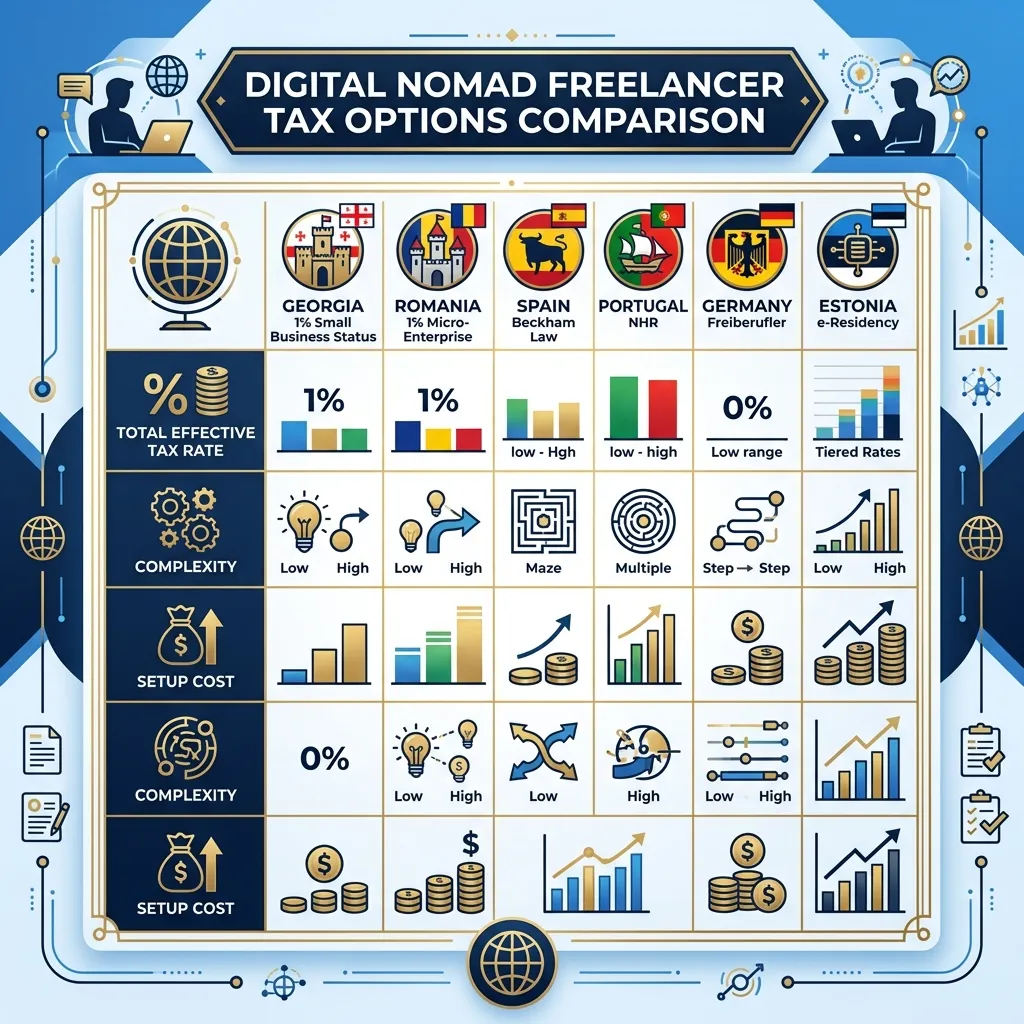

How Does Portugal Compare to Other Digital Nomad Tax Destinations?

| Country | Tax Regime | Rate | Duration | Key Requirement |

|---|---|---|---|---|

| Portugal (NHR) | Flat rate | 20% | 10 years | 5 years non-residency |

| Greece (50% exemption) | Income discount | 4.5%–22% effective | 7 years | 7 of 8 years abroad |

| Georgia (Small Business) | Flat rate | 1% | Ongoing | Revenue under GEL 500k |

| UAE/Dubai | Zero tax | 0% | Ongoing | Residency visa |

| Spain (Beckham Law) | Flat rate | 24% | 6 years | Not resident in prior 5 years |

| Italy (Inpatriate) | 70% exemption | ~8.6% effective | 5 years | 2 years non-residency |

Pros and Cons of the NHR Regime

Advantages

- Significant tax savings — The 20% flat rate delivers major savings for earners above €35,000

- Foreign income exemptions — Dividends, interest, and capital gains from DTA countries can be fully exempt

- 10-year guarantee — Once approved, your rates are locked in for a decade

- Quality of life — Portugal offers excellent weather, safety, affordable cost of living (outside Lisbon), and a thriving digital nomad community

- EU residency — Access to the Schengen area and EU single market

Disadvantages

- Social security costs — These are not reduced under NHR and can add 10–15% to your effective tax burden

- Narrower eligibility (NHR 2.0) — The 2024 reforms restrict qualifying activities compared to the original program

- 5-year non-residency rule — If you’ve lived in Portugal recently, you won’t qualify

- Bureaucracy — Portuguese administrative processes can be slow and documentation-heavy

- Cost of living in Lisbon/Porto — Major cities have become expensive, with average rents of €1,200–€2,000/month for a one-bedroom apartment

Frequently Asked Questions

Can I apply for NHR if I’ve lived in Portugal before?

You cannot apply if you were a Portuguese tax resident in any of the five years preceding your application. If you left Portugal more than five years ago and have not been tax resident since, you can reapply.

Does NHR apply to crypto income?

Crypto gains in Portugal have undergone regulatory changes. As of 2026, short-term crypto gains (held less than 365 days) are taxed at 28% regardless of NHR status. Long-term gains (held over 365 days) remain exempt. NHR does not provide additional benefits for crypto taxation.

What happens after the 10-year NHR period expires?

Once your 10-year NHR period ends, you revert to Portugal’s standard progressive tax rates (14.5%–48%). Many NHR holders use this transition to reassess their tax residency strategy. Planning ahead is essential — consider consulting a tax advisor during year 8 or 9 of your NHR.

Can I combine NHR with the Portugal Digital Nomad Visa?

Yes. The D8 Digital Nomad Visa grants you legal residency in Portugal, and once you establish tax residency, you can apply for NHR status. The D8 visa requires proof of minimum monthly income of €3,510 (four times the Portuguese minimum wage).

Do I need to declare worldwide income under NHR?

Yes, NHR holders must declare their worldwide income in their annual Portuguese tax return. However, qualifying foreign income may be exempt from taxation or taxed at preferential rates depending on the income category and the applicable DTA.

Is NHR worth it for low-income digital nomads?

For income below approximately €25,000–€30,000, the standard progressive rates may actually be more favorable than the 20% NHR flat rate. The crossover point depends on your deductions and personal situation. Run your numbers through our Tax Calculator to find out.

Final Thoughts

Portugal’s NHR regime remains one of Europe’s most competitive tax frameworks for digital nomads and remote professionals, even after the 2024 reforms. The 20% flat tax rate on qualifying income, combined with potential exemptions on foreign-sourced earnings, can result in substantial savings compared to both Portuguese standard rates and many other European countries.

However, the regime is not a one-size-fits-all solution. Social security costs, the narrower eligibility under NHR 2.0, and Lisbon’s rising cost of living are all factors to weigh carefully. For a personalized estimate of your tax liability under the NHR regime, try our Tax Calculator — it models Portuguese taxation alongside other popular digital nomad destinations.

The key is to plan early, gather your documentation, and ideally work with a qualified Portuguese tax professional to ensure a smooth application and maximize your benefits over the full 10-year period.